Ever wondered how the Federal Reserve interest rates impact your wallet? It's not just some fancy financial jargon—it's a big deal that affects everything from your mortgage payments to your credit card bills. Imagine the Federal Reserve as the conductor of the U.S. economy's orchestra, and interest rates are the melody that keeps everything in sync. But what happens when the melody changes? Let's dive in and find out.

You might be thinking, "What does the Federal Reserve even do?" Well, buckle up because this ain't just about boring numbers. The Fed, as it's commonly called, has a massive role in steering the economic ship. And one of their main tools? You guessed it—interest rates. They're like the volume control for the economy, and when they crank it up or down, everyone feels the effects.

So why should you care? Because the decisions made by the Federal Reserve don't just affect Wall Street—they hit Main Street too. Whether you're saving for retirement, trying to pay off debt, or looking to buy a house, understanding how these rates work can be a game-changer. Let's break it down and make sense of the financial landscape together.

Read also:Hd Hub 4u Your Ultimate Destination For Highquality Content

What Are Federal Reserve Interest Rates Anyway?

Alright, let's start with the basics. Federal Reserve interest rates, often referred to as the "fed funds rate," are the interest rates banks charge each other for overnight loans. Think of it like a club where banks lend money to each other to meet their reserve requirements. The Fed sets a target range for this rate, and it's a key tool they use to influence the economy.

Here's the kicker: when the Fed adjusts these rates, it ripples through the entire financial system. Lower rates mean cheaper borrowing costs for consumers and businesses, which can stimulate spending and investment. On the flip side, higher rates can slow down the economy by making borrowing more expensive. It's all about finding that sweet spot to keep inflation in check while promoting growth.

Why Do They Matter to You?

Let's get real for a sec. These rates aren't just some abstract concept—they hit close to home. For example, if you have a variable-rate mortgage, your monthly payments could go up or down depending on what the Fed does. Same goes for credit card interest rates and car loans. It's like the Fed has their fingers on the pulse of your financial life.

And it's not just about personal finance. Businesses also feel the pinch. When borrowing costs rise, companies may delay expansions or hiring, which can affect job opportunities. It's a domino effect that touches every corner of the economy.

How Federal Reserve Interest Rates Affect the Economy

The Fed's interest rate decisions are like the thermostat for the economy. They can turn the heat up or down depending on the economic climate. During a recession, the Fed might lower rates to encourage borrowing and spending, which can help jumpstart growth. Conversely, if the economy is overheating and inflation is running wild, they might raise rates to cool things down.

This balancing act is crucial because too much inflation can erode purchasing power, while too little can lead to stagnation. The Fed aims for a "Goldilocks" economy—not too hot, not too cold, but just right. And interest rates are one of their primary tools to achieve that balance.

Read also:Hdhub4u 4k Your Ultimate Destination For Highquality Streaming

Interest Rates and Inflation: The Dynamic Duo

Inflation is like the Fed's kryptonite. If it gets out of control, it can wreak havoc on the economy. That's why the Fed keeps a close eye on inflation trends when setting interest rates. When inflation rises, they might hike rates to reduce spending and borrowing, which can help bring prices back down to earth.

On the flip side, if inflation is too low or deflationary pressures emerge, they might lower rates to encourage more economic activity. It's a delicate dance, and the Fed has to be nimble to stay ahead of the curve.

Historical Context: How We Got Here

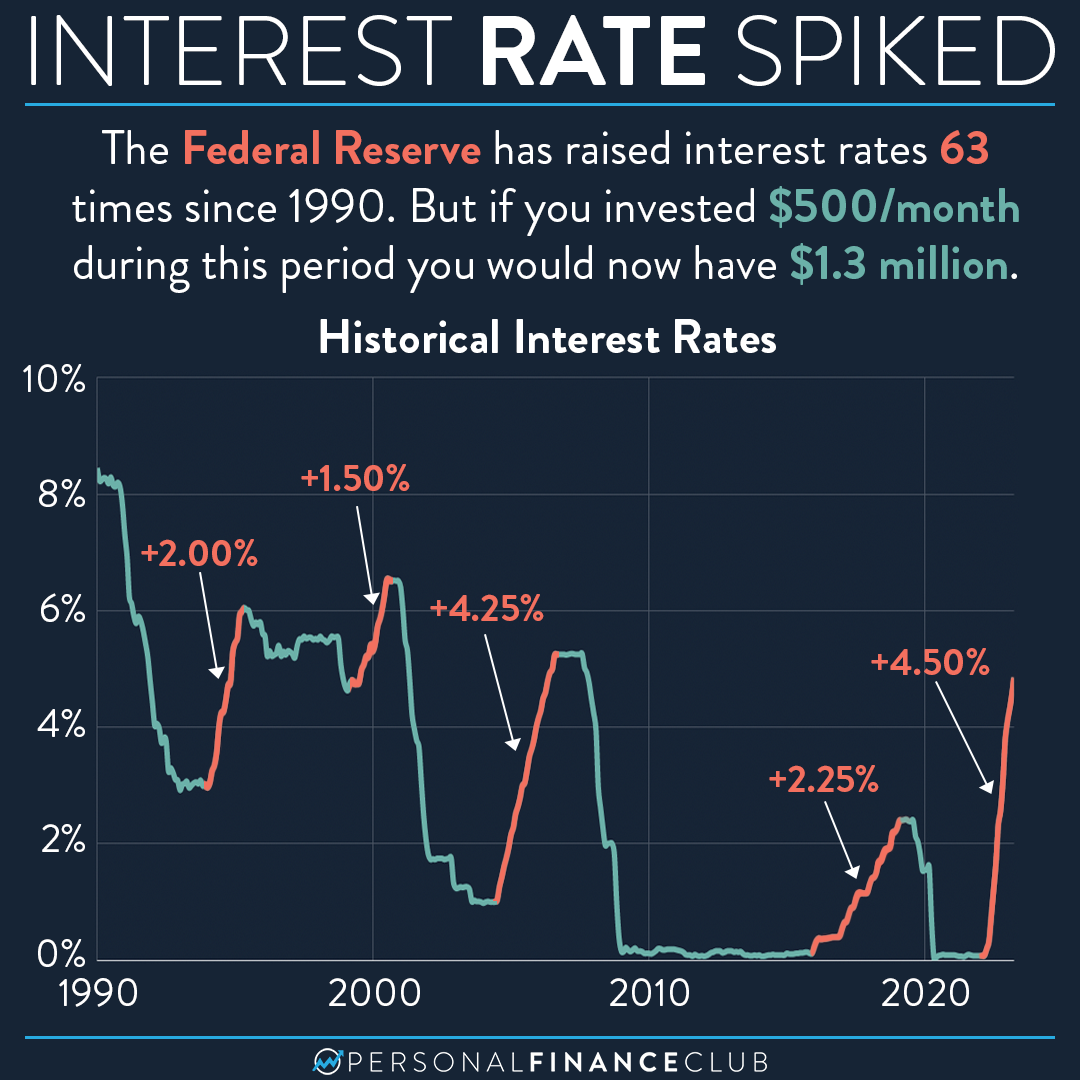

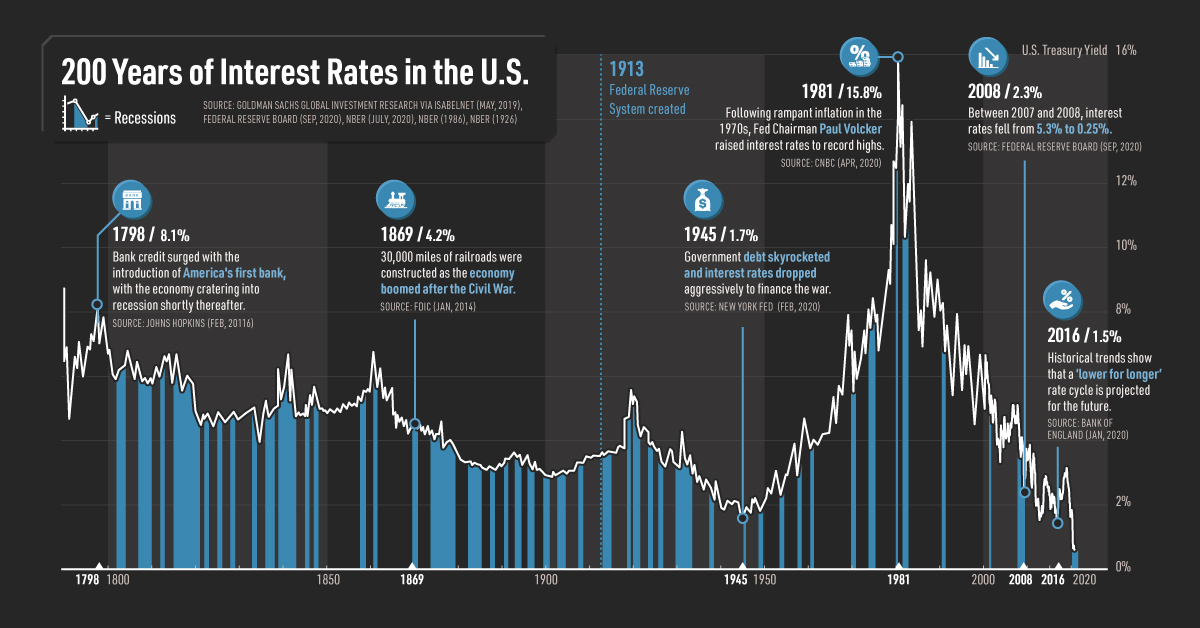

To truly understand the impact of Federal Reserve interest rates, it helps to look back at history. The Fed has been around since 1913, but its role has evolved over time. One of the most memorable periods was the 1970s, when inflation spiraled out of control. The Fed had to take drastic measures, hiking rates to unprecedented levels to rein in prices.

Fast forward to the 2008 financial crisis, and the Fed found itself in uncharted territory again. They slashed rates to near zero and implemented unconventional policies like quantitative easing to stabilize the economy. It was a bold move that some criticized, but it helped prevent a deeper downturn.

Lessons Learned from the Past

History teaches us that the Fed's decisions have far-reaching consequences. Whether it's navigating a recession or managing an inflationary spike, their actions shape the economic landscape for years to come. By studying these historical examples, we can better understand the rationale behind their current policies.

And let's not forget the human element. Millions of people's lives were impacted by the Fed's actions during those turbulent times. From job losses to housing market crashes, the ripple effects were felt across the nation. It's a reminder of the weight that rests on the Fed's shoulders.

The Federal Reserve's Dual Mandate

Now, here's where things get interesting. The Fed has a dual mandate: to promote maximum employment and stable prices. These two goals sometimes conflict, and finding the right balance is no easy feat. For example, lowering rates to boost employment might lead to higher inflation, while raising rates to control inflation could slow job growth.

This dual mandate is enshrined in law, and it guides the Fed's decision-making process. But it's not just about numbers—they also consider qualitative factors like economic trends and global developments. It's a complex puzzle that requires a lot of brainpower to solve.

Challenges in Balancing the Mandate

Striking the right balance between employment and inflation is easier said than done. External factors like geopolitical tensions, natural disasters, and pandemics can throw a wrench in the works. The Fed has to be agile and adapt to changing circumstances while staying true to its mandate.

And let's not overlook the political pressures they face. The Fed is an independent entity, but that doesn't mean they're immune to criticism. Policymakers, businesses, and the public all have opinions on what the Fed should do, and those voices can be loud and influential.

How Federal Reserve Interest Rates Impact Investments

Investors, take note—interest rates have a big impact on the markets. When rates rise, borrowing costs increase, which can weigh on corporate profits and stock prices. On the flip side, lower rates can fuel a rally as companies and consumers have more money to spend.

Bonds are particularly sensitive to rate changes. When rates go up, existing bonds with lower yields become less attractive, causing prices to fall. Conversely, when rates drop, bond prices tend to rise. It's a seesaw effect that keeps investors on their toes.

Strategies for Navigating Rate Changes

So how can you protect your portfolio in a changing rate environment? Diversification is key. Consider a mix of asset classes that perform differently under various rate scenarios. For example, some investors might favor dividend-paying stocks or real estate investment trusts (REITs) in a rising rate environment.

It's also important to stay informed and adjust your strategy as needed. The markets can be unpredictable, and reacting too quickly or too slowly can be costly. Work with a financial advisor if you're unsure about the best course of action.

What's on the Horizon for Federal Reserve Interest Rates?

Looking ahead, the Fed faces a host of challenges. Global economic uncertainty, supply chain disruptions, and shifting demographics are just a few of the factors they must consider. Add to that the ongoing battle against inflation, and you've got a recipe for some tough decisions.

Some experts predict that rates will remain elevated for the foreseeable future as the Fed works to bring inflation under control. Others believe that a slowdown in economic activity might prompt them to ease up on the brakes. Only time will tell which scenario unfolds.

Key Factors to Watch

To get a glimpse into the Fed's thinking, keep an eye on key economic indicators like the unemployment rate, consumer price index (CPI), and gross domestic product (GDP). These metrics provide valuable insights into the health of the economy and can signal potential shifts in monetary policy.

Also, pay attention to the Fed's public statements and meeting minutes. They often hint at their future plans and provide context for their decisions. Staying informed can help you anticipate changes and make more informed financial decisions.

How to Prepare for Changing Rates

Whether you're a consumer, business owner, or investor, there are steps you can take to prepare for changing interest rates. Start by reviewing your debt situation. If you have variable-rate loans, consider refinancing to a fixed rate while rates are still relatively low.

For savers, it might be worth exploring high-yield savings accounts or certificates of deposit (CDs) that offer better returns in a rising rate environment. And if you're in the market for a new home or car, timing your purchase wisely can save you thousands in interest payments.

Building a Resilient Financial Plan

A solid financial plan is your best defense against the uncertainties of the market. Work with a trusted advisor to create a strategy that aligns with your goals and risk tolerance. Regularly review and adjust your plan as needed to stay on track.

Remember, the Fed's actions are just one piece of the puzzle. A well-diversified portfolio, emergency savings, and a long-term perspective can help you weather any storm that comes your way.

Conclusion: Take Control of Your Financial Future

In conclusion, Federal Reserve interest rates play a pivotal role in shaping the economy and influencing your financial decisions. By understanding how they work and staying informed, you can make smarter choices about borrowing, saving, and investing.

So what's next? Take action! Review your financial situation, educate yourself on the markets, and don't be afraid to seek professional advice if needed. Together, we can navigate the complexities of the financial world and build a brighter future for ourselves and our families.

Don't forget to share this article with your friends and family. Knowledge is power, and the more we understand about the forces shaping our financial lives, the better prepared we'll be to thrive in any economic climate.

Table of Contents

- What Are Federal Reserve Interest Rates Anyway?

- Why Do They Matter to You?

- How Federal Reserve Interest Rates Affect the Economy

- Historical Context: How We Got Here

- Lessons Learned from the Past

- The Federal Reserve's Dual Mandate

- Challenges in Balancing the Mandate

- How Federal Reserve Interest Rates Impact Investments

- Strategies for Navigating Rate Changes

- What's on the Horizon for Federal Reserve Interest Rates?